Award-winning PDF software

Printable Form 8288 San Diego California: What You Should Know

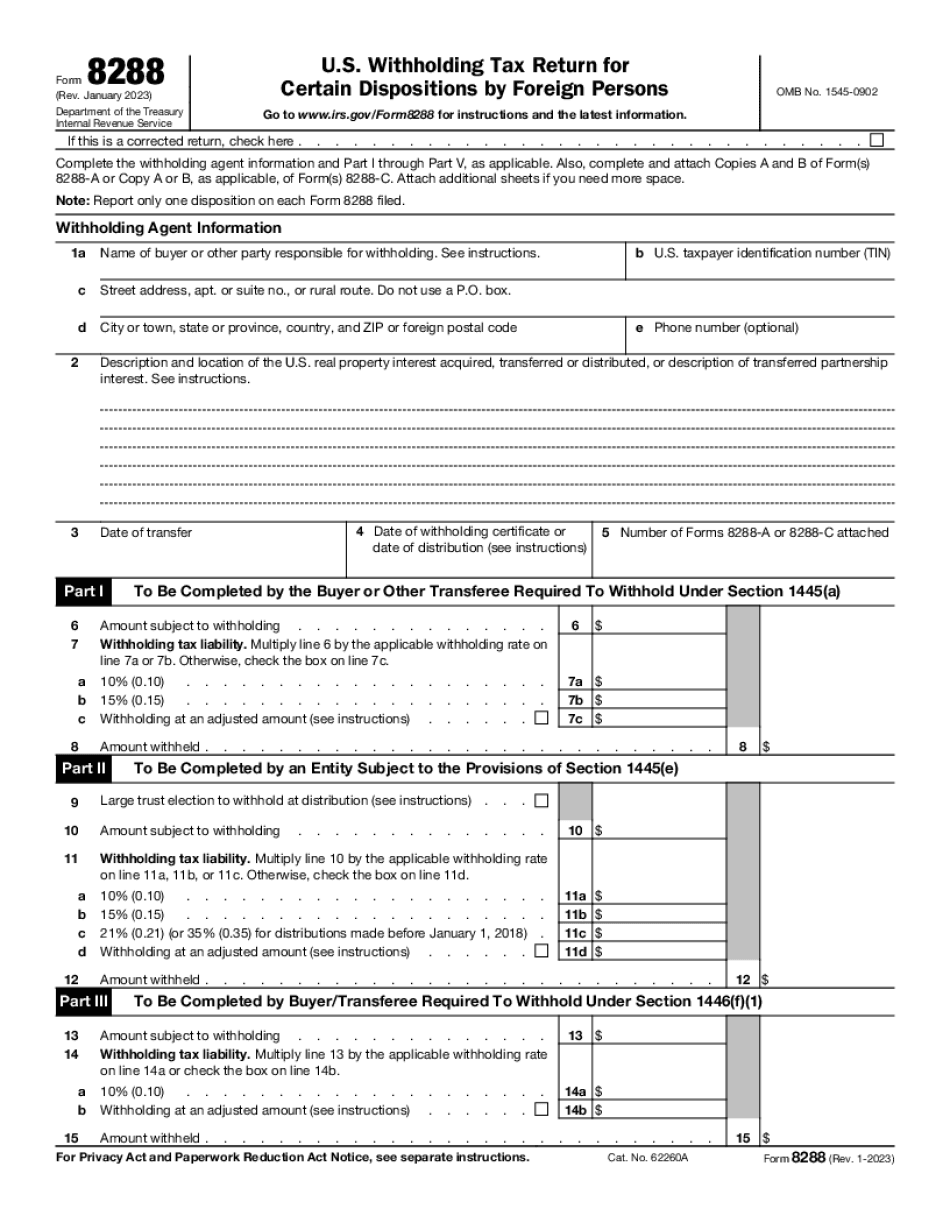

For the California reporting state, the form title will be changed to conducted in San Died, CA. For the Federal reporting state, the form title and paragraph are unchanged with the addition of the state, and it will be reviewed in the Federal Register. It may become effective on January 1, 2023. The changes to the 8288 Form have been approved by the IRS and are effective as of 7/11/2018. “This is a significant change from previous UCR reports.” The Treasury Inspector General for Tax Administration said in a press release. “This change results in the addition of new reporting requirements that are based on the new California reporting state. This new state will require reporting of the California taxpayer's foreign tax credits in the current U.S. Form(s) 8288 and any other applicable tax returns from the foreign person.” In California, California taxpayers are no longer subject to filing California income tax withholding on qualified dividends received by foreign persons. They are now expected to self report such dividends in a Form 1099-DIV (Electronic Data Interchange). “The new information required by California will now also need to be entered on an IRS form called the Withholding Forgiveness Letter when the taxpayer wishes for his or her foreign tax credit. This form will be mailed to the taxpayer with the refund check on December 31 of each year.” “This is a great improvement in California reporting and will be very valuable for California taxpayers, but it is only good for the rest of the country. For example, when the taxpayer receives the Form 1099-DIV, that tax is not automatically transmitted to the California state income tax. Instead, the taxpayer would have to submit another Form 8288 to the IRS for that information.” As of March 2018, California taxpayers are required to report their tax paid on qualified non-domiciled dividends received by foreign persons. Foreign persons receiving qualified dividends that are received or held in California are required to file a California income tax withholding on those dividends on the same basis as income received by a resident of California. Individuals not reporting dividends to or received from a controlled foreign corporation are no longer subject to tax at source when dividends received in a single State are distributed by that corporation to all or substantially all its employees and shareholders outside of California. “In addition, the income tax information is no longer required after the first payment of dividends.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Printable Form 8288 San Diego California, keep away from glitches and furnish it inside a timely method:

How to complete a Printable Form 8288 San Diego California?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Printable Form 8288 San Diego California aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Printable Form 8288 San Diego California from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.