Award-winning PDF software

Springfield Missouri Form 8288: What You Should Know

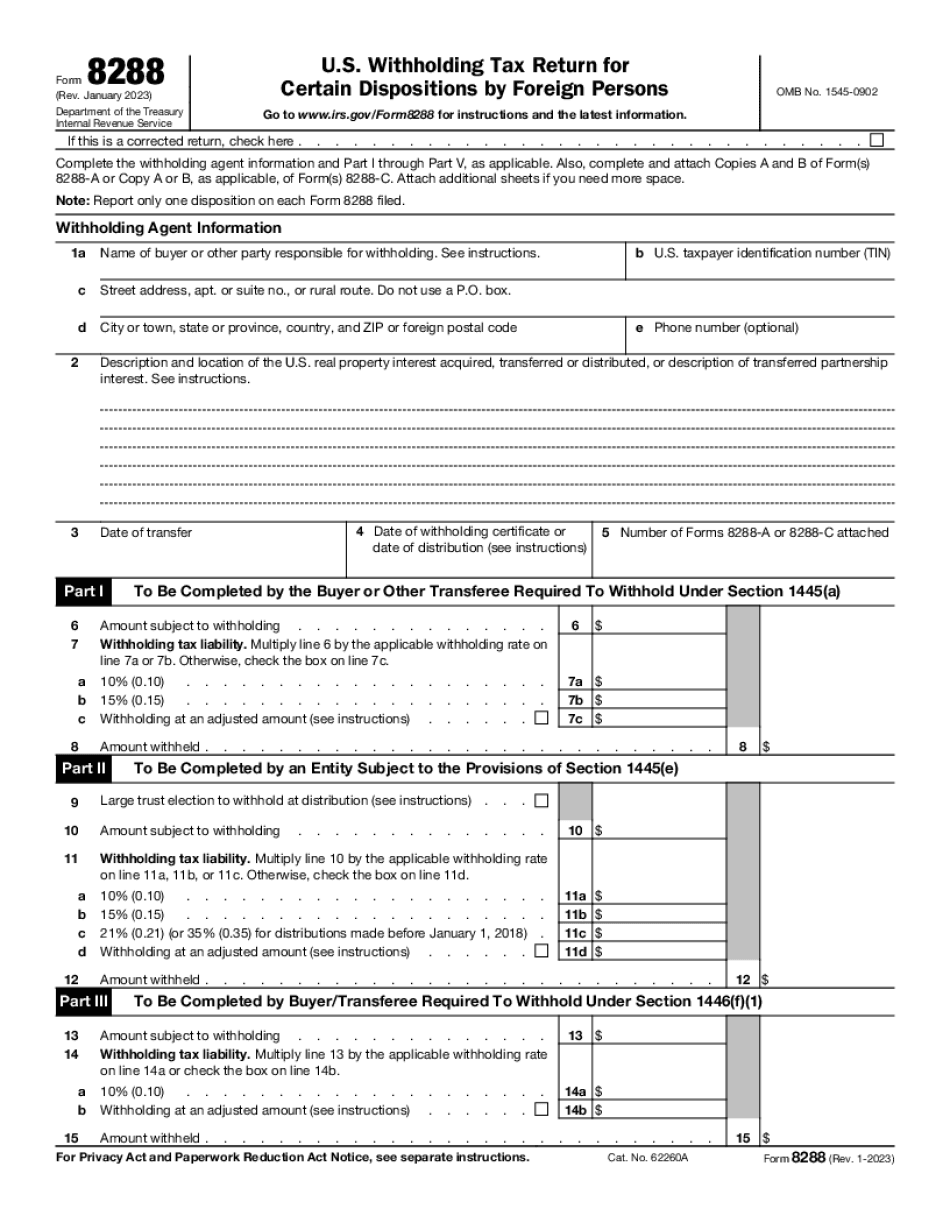

The information required can also be found on other IRS publications, especially those about interest and dividends by individuals. Interest and Dividends by Individuals and Foreign Persons You should carefully read IRS Publication 587 to help you interpret the instructions for Form 2555, Interest and Dividends by Individuals and Foreign Persons. Interest and Dividends by Individuals. What Is Interest? Interest is the periodic payment of interest on a capital asset. The payment may be made in one or more installments. Interest on bonds and certain bonds denominated in foreign currencies usually is paid semi-annually. Interest paid on foreign currency bonds is usually paid annual. Interest on bank deposits and certain long-term contracts is paid semi-annually. Interest (or the earnings on capital) is not a part of compensation for work performed as defined in section 162 of the Internal Revenue Code (IRC). Interest is generally taxable when: • the payment exceeds the amount actually received; • no tax liability would result if payments for the year had continued the same; or • the payment exceeds the tax liability, if any, attributable to that portion of the payment that exceeds the amount of that liability. Interest on certain income, net of allowable deductions, is subject to taxes in the same manner as ordinary income. (There are tax consequences even if the amount is reduced under other conditions.) Interest is generally subject to taxes with advance payment. On the taxpayer's written request the IRS will allow advance payment of interest in such amounts as may not exceed 20% of the amount due. Interest is generally subject to a 20% tax on the first 2,000 of interest due. The tax rate for subsequent amounts is the highest of: -25% of the tax for the first 2,000; or -0% for amounts exceeding the first 2,000. No additional tax due. Taxpayers may also deduct the interest paid. The net interest paid may reduce the tax on the payment and/or may offset any interest deductible otherwise. The “interest” paid on this form of payment is income or gain that is subject to tax. If the interest is received by a United States national for employment purposes, the taxpayer is the (payer) of the interest. Dividends on stock are taxable to the mayor on the dividend or the amount received. The dividends, if not subject to withholding and received as described in Pub. 597, Interest on Unearned Income, would generally be tax-free.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Springfield Missouri Form 8288, keep away from glitches and furnish it inside a timely method:

How to complete a Springfield Missouri Form 8288?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Springfield Missouri Form 8288 aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Springfield Missouri Form 8288 from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.