Award-winning PDF software

Form 8288 Minneapolis Minnesota: What You Should Know

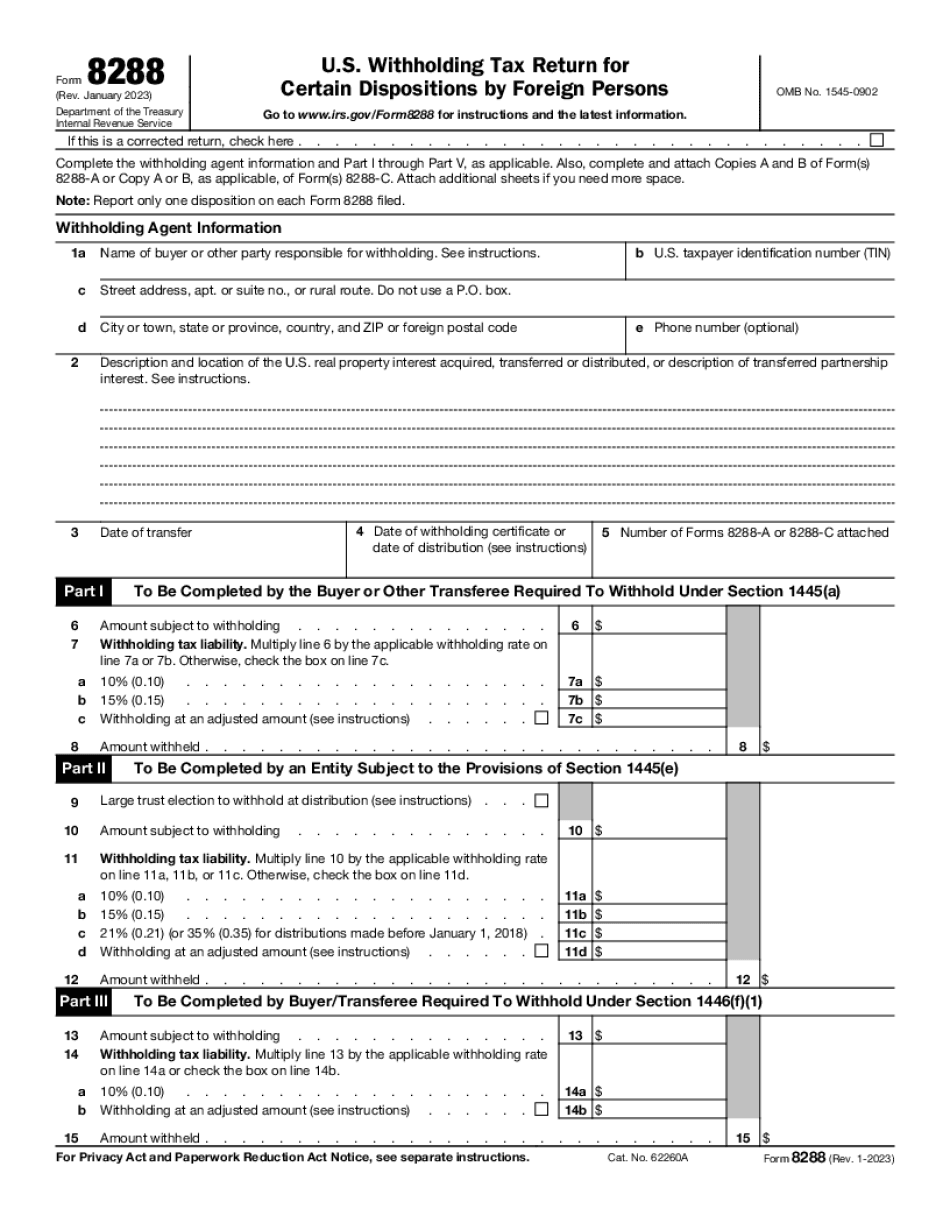

S. Real property interest for consumption purposes, a single return to the non-resident alien investor will not be filed by the foreign person. However, the seller has to file separate returns for each individual investor/owner. Q6 If a foreign person is a U.S. person that engages in any business related to real estate which includes real property owned by one or more U.S. persons, and is not a qualified corporation or a partnership (unless it is a qualified domestic corporation), then, no separate returns will be filed. Q7 A taxpayer must file a separate, self-contained return for each investment in real property. Individuals and Entities | Minnesota Department of Revenue Information about Form 8287, U.S. Person's Withholding From Foreign Sources on Individual Property Interested in U.S., including recent updates, Instructions for Form 8287 (Rev. December 2019) — Minnesota Department of Revenue An investor should file a separate paper return for each sale to which the individual property interest is related. A resident, alien or non-resident may be subject to U.S. withholding as the result of ownership by a non-resident who acquires U.S. real property interest for consumption purposes. The amount that the non-resident's own income must be withheld can be calculated under this item : (a) For income tax withholding on income from real property interests, see IRS Publication 519: IRS Withholding on Income from Real Property Interests. As an individual taxpayer, the individual income tax, Medicare tax and self-employment tax is generally withheld from all net income from U.S. real property interests held in the year of purchase. The withholding rules set forth in section 1431A are used in the computation of the U.S. person's federal income tax withholding liability. The withholding rules in Part IVA of Publication 519 are modified in part to use the actual gain or loss in determining the U.S. person's federal income tax withholding. The actual gain or loss is computed under the general principles that the U.S. person's interest in the property is treated as a capital asset for U.S. federal income tax purposes. The amount of allowable withholding is limited to the least of the amount of income tax withheld on the income and gain from the disposition of the property and the total of the U.S.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8288 Minneapolis Minnesota, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8288 Minneapolis Minnesota?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8288 Minneapolis Minnesota aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8288 Minneapolis Minnesota from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.