Meet John. John owns a vacation home in the US. He wants to sell his home, but he's not a US citizen or a US resident. As a foreigner, John has to deal with FERPA. Meet Mike. He wants to buy John's house. Since John is a foreigner, now Mike has to deal with FERPA too. So, what is FERPA? FERPA is a withholding tax. Withholding is an amount that is set aside to pay for potential taxes down the road. Think of it as an advanced tax payment. When John sells his property, he will be earning US income. When he earns US income, he has to pay an estimated tax payment on that income. That estimated tax payment will stay at the IRS until John files a US tax return. If he ends up owing less than what was paid in advance, then he will get a refund of the difference. Collecting the payment upfront is the only way the IRS can make sure that John files his tax return. But how does the IRS go about collecting that payment? Remember Mike, when Mike buys John's house, he will need to hold back 15% of the selling price and make a payment to the IRS on John's behalf. If he doesn't, he might have to pay the 15 percent himself. John called the specialists at FERPA Solutions. They explained the process and his option to either remit or apply for a withholding certificate. John didn't have a US tax ID, so FERPA Solutions helped him to apply for one. A few short months later, John has his 15% back in his bank account where it belongs. So, whatever happened to Mike? Well, Mike went on to live a happy life in his brand-new home. He never heard from...

Award-winning PDF software

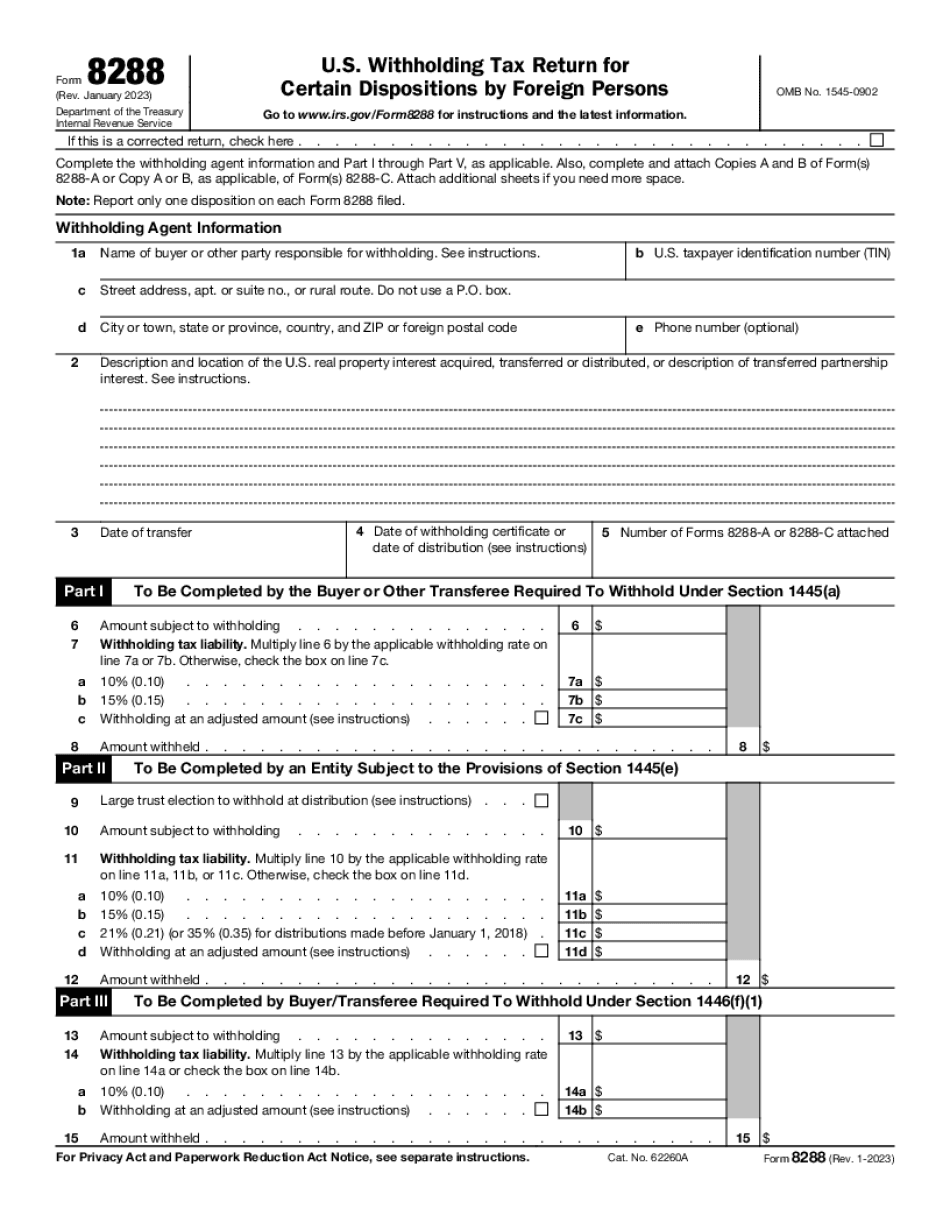

Firpta section 1445 Form: What You Should Know

The reduction (or credit) shall be applied against any income tax, special assessment, or special rate. (3) Special rules for transfers of real property to spouses with U.S. tax liability. If the transfer is made on or after the date of enactment of this paragraph, only the foreign person's tax on the transferred real property, if any, will be subject to income tax withholding when the transferee (buyer) takes a gain in a participating security. If the transfer is made before the date of enactment of this paragraph, the transferor's tax on the transferred real property, if any, will be subject to income tax withholding only when the transferee (seller) takes a gain in the underlying participating security. For transfers of tangible property, such as land, to U.S. citizens, permanent residents (nonresidents) or corporations with U.S. tax liability, the transferor must pay or reimburse the transferred property with respect to U.S. tax withheld. For transfers of tangible property to all other persons to which income is attributable, whether income is included, tax on the transferred property will be credited to the transferor's income tax or withholdable portion of the gross income of the transferred property and any gain realized on such a transfer. This exception does not apply to a transfer in connection with an involuntary conversion or to transfers from a U.S. holding company to a foreign holding company on a tax basis. 26 U.S. Code § 906 — Taxation of gains derived from sales of controlled foreign corporations.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8288, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8288 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8288 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8288 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Firpta section 1445